The Quarterly Checkup

Q2 2024 Market & VC Landscape

Monday, 15 October 2024 I Written by Jason Robertson

Market Overview

Mixed signals. That was the title of a recent article on the state of VC in Q2 and I think it is apt to describe the current environment – VC and otherwise. Last quarter I shared with you that continued inflation in Q1 was reducing the market’s expectations of rate cuts in 2024 – some even suggesting rate hikes may be on the table. Fast forward one quarter and now, given slowing inflation and worrisome employment data, prognosticators are thinking a 50-bps cut (or a double rate cut) may happen in September with 100-bps worth of cuts before year-end and that the Federal Reserve may have waited too long to respond to deteriorating economic data. Regardless, the S&P 500 has shrugged this off and continued its relentless march upwards increasing almost 15% in the first half of 2024 and hitting a high of almost 20% in mid-July before falling back 10% on a spate of worrying economic data and the unwinding of the yen-dollar trade. The volatility index, the VIX, spiked 4x in one day as Japan’s Nikkei index tanked 20% followed by Wharton professor Jeremy Siegel’s public outcry that an emergency 75 bps rate cut was need. As of this report, the VIX is back down to normal levels and the stock market is going up again.

Somewhat incongruently, public markets are seemingly beginning to weary of the AI narrative and are rotating out of the magnificent 7 (or at least taking profits on the run-up this year) into the S&P 493. Yet, Warren Buffett, through Berkshire Hathaway, has amassed almost $300B in cash, a sign many interpret as his belief that stocks are overvalued and that he’s readying his “elephant gun” for better opportunities ahead following a market correction. And in venture, the same appears true: flat and down rounds hit a decade high, while median late-stage valuations are surpassing the 2021 bull market. In this market, it’s understandable and easy to feel confused.

The exit markets for VCs remain challenged despite some notable IPOs and acquisitions in 2024, including Rubrik’s and Ibotta’s public debuts in Q2; however, post-IPO performance of those companies has been lackluster. Private unicorn counts and values continue to hit decade-highs and M&A, which makes up the majority of liquidity events, has experienced a steep decline in activity as increased regulatory scrutiny has combined with shareholder activism around accretive acquisitions to make the environment frosty. Furthermore, many unicorns are holding back from attempting to join public markets in this uncertain climate, leading the median portfolio company age to hit decade-highs. Furthermore, VC-backed IPO price/sales multiples sit at decade lows at 4.9x. Thus, returning capital to LPs has required GPs to seek more creative solutions and the only reliable opportunities for exits in this environment have been buyouts (at 10-year highs) and secondaries (also demonstrating significantly increased activity).

Secondaries have been an important part of liquidity for VCs in recent years and the latest data suggests that discounts due to supply/demand imbalances bottomed out in early 2023 and prices are moving towards parity with the last round; however, deep discounts of ~30% are still the norm – a far cry from the 10-20% premiums prior to 2022.

In Canada, inflation come in at 2.5% for July, in-line with expectations, down from 2.7% in June and 2.9% in March further moderating prices since the beginning of 2024. This has led markets to increase the probability of a third rate cut by the Bank of Canada (BoC) following the two 25 bps cuts earlier this year. Though we had speculated that Canada’s advanced rate cuts next to the Fed might negatively impact the Canadian dollar, expectations of 1-2 rate cuts in the US in September seem to be towing the line.

In summary: mixed signals. Although we expect more clarity and directionality in H2, especially around the economy and the new President of the United States, things remain on a tinder box with the potential for massive volatility should something happen – or not happen – that the markets didn’t anticipate.

VC Ecosystem Overview

The venture market in Q2 displayed modest improvements, the continued uptick in deal count and deal value providing some glimmers of hope, but it is still too early to call it a rebound. The data validates our anecdotal conversations with other VCs that Q1 deal flow was robust; however, it seems that deals took longer to complete than usual. Although surface Q2 numbers may paint a rosier picture with $55.6B invested across 4,226 deals – reasonably higher than the pre-pandemic steady state and the best quarter since 2022 – the details demonstrate that a few outlier deals were significant contributors. Megadeals in particular accounted for more than half at $34.1B and two deals (CoreWeave and xAi) accounted for almost $15B. This supports our belief that completed deals are larger than typical as VCs proclaim their preference for experienced founders and plowing more money into fewer deals.

Q2 2024 again demonstrated investor-friendliness in the current macro environment; however, it also highlighted that VCs have slowed their deployment pace to extend their existing funds while they try and achieve DPI before raising a subsequent fund. Consequently, most VCs are investing more resources (time and money) with existing portfolio companies and helping them chart a course through difficult markets. Thus, deals are taking longer to close, more due diligence is being undertaken, and hurdles have increased to deploy capital.

Given this heightened selectivity, a lack of exit opportunities for startups, and the abysmal fundraising environment over the last two years, it is no surprise that data from Carta paints a bleak picture of Q1 2024: startup shutdowns on Carta hit their highest level – a 58% increase from 2023 after a 124% jump between the first quarters of 2022 and 2023. That said, context is required here and these are absolute figures whereas Carta’s customer base has grown substantially in 4 years so this says nothing of proportionality. However, it is reasonable to expect that as data for the remainder of the year trickles in, this trend will remain present. Furthermore, given the time it takes for startups to “close” once operations cease (usually >1 year for tax purposes), it is possible this is just the tip of a much larger iceberg.

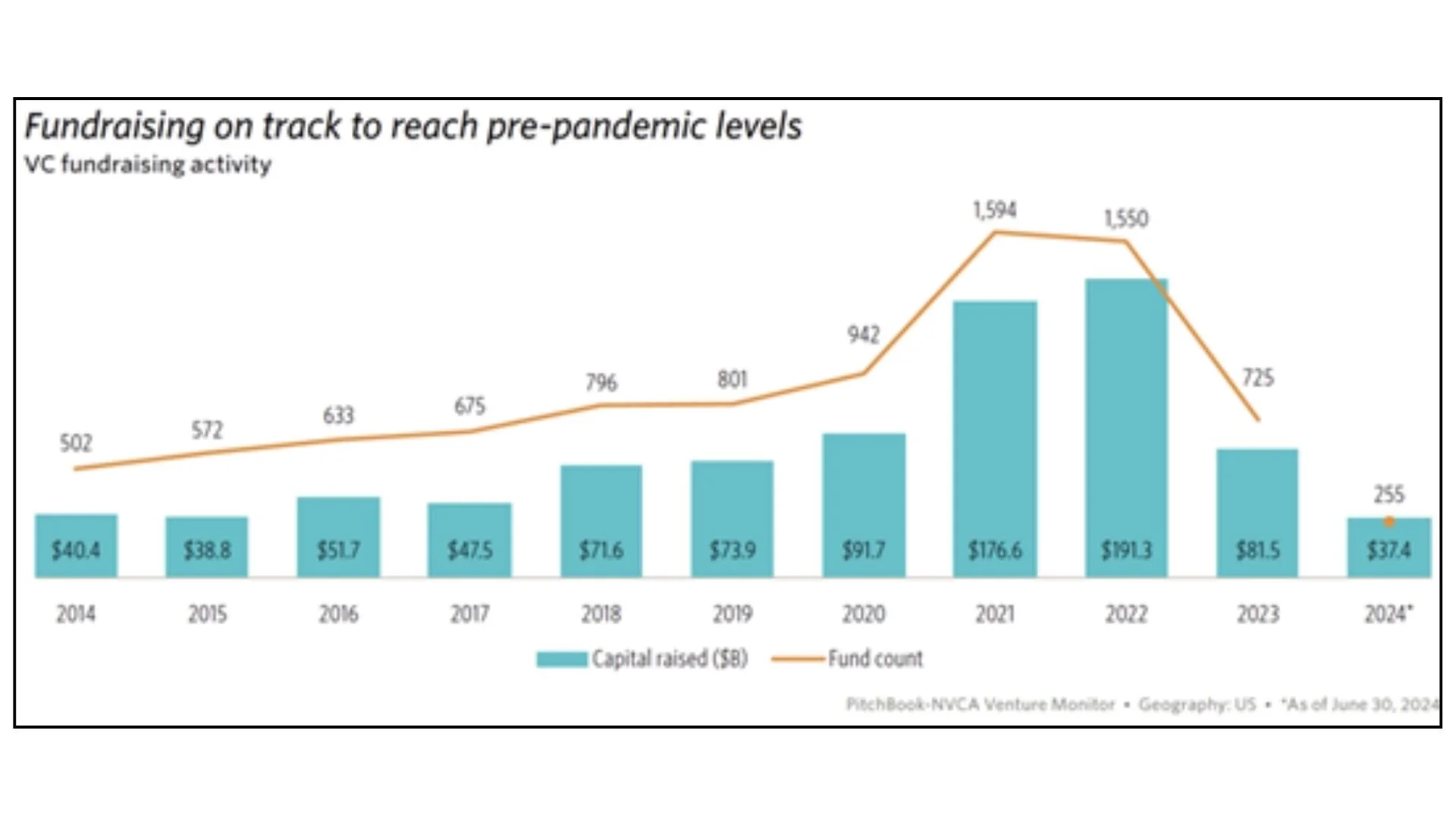

As highlighted earlier, the lack of liquidity for GPs is hurting LP distributions and disrupting financing models thereby preventing LPs from committing to new funds. This trend is illustrated by the VC 12-month distribution yield as a percentage of net asset value (NAV) for funds aged five to 10 years, which fell to a near low of 5.1% in Q2, well below the 10-year average of 17.1%. With only $37.4B committed to 255 funds YTD, 2024 may be the worst VC fundraising year since 2017.

Record-high VC dry powder of $296.2B persists in Q2 although some drawdown has seemingly occurred relative to Q1’s $312B. 58% of this dry powder is held in funds with commitments exceeding $500 million, and 67% is allocated to funds from 2020-2022. Established managers continue to secure the substantial majority (77%) of new capital raised so far this year with over 63% allocated in funds >$500M in size. As with startups, LPs are spending more time on due diligence in the slow environment to identify the best GPs with unique skills, durable competitive advantages, and strong track records that differentiate themselves. That said, even brand name firms are struggling to raise new funds with many household names closing funds a fraction of the size of their prior funds.

Emerging managers are facing even greater hurdles due to hesitant LPs. Through Q2, despite similar fund counts, emerging funds raised $8.6 billion, compared with experienced funds, which raised $28.8 billion. Although not surprising in this risk-off atmosphere, LPs preferences fly in stark contrast to the clear 30-year+ historical data that shows emerging managers meaningfully outperform established managers… but with heightened volatility.

VC Early Stage Overview

In Q2, $3.3B was deployed in pre-seed and seed stage deals representing an uptick in deal value from Q1’s $2.6B. Furthermore, the trend of increased round sizes continued in Q2, which had the fewest sub-$1 million pre-seed/seed deals as a share of all pre-seed/seed deals since 2015. Commensurately, pre-seed/seed deals valued >$10M as a percentage of overall pre-seed/seed deals hit the highest level ever. Again, this represents a flight-to-quality by investors where more money is being invested into fewer ventures and consequently at higher valuations to ingest that increased amount of capital. While inflation may be a contributor, technology is also deflationary and thus we expect these to be somewhat offsetting.

VC Digital Health Overview

US digital health funding in Q2 2024 moved up slightly from Q1’s $2.7B to $3.0B (up ~11% from Q1) across 133 deals (flat from Q1), with an average deal size of $22.2M (up ~8%). While average cheque sizes were up from Q1, they remain depressed reflecting 2018/2019 values. Despite our reservations that Q1’s relative strength wouldn’t continue through the year, Q2 was more robust than anticipated but once again reinforced deal volume consistency over the last two years. Early-stage deals (Seed, A, B) were responsible for 84% of deals in Q2 with Series A notably strong as marquee deals with Zepher AI ($111M), Allez Health ($60M), and Fabric ($60M) pushed values up.

As anticipated from prior quarters, Q2 notched a notable decrease in unlabeled rounds of “only” 33% compared to Q1’s 47% and 55% in Q4 2023. This dwindling of “transitionary” rounds may point to a return to a more “normal” fundraising environment – although “normal” historically was closer to single-digit percentages (e.g. 4% in 2019).

After almost 2 years without a public debut, three digital health companies IPO’d in Q2 reflecting the broader modest uptick in IPOs for tech companies: remote fetal monitoring platform Nuvo; revenue cycle management company Waystar; and, precision diagnostics player Tempus AI. However, these public exits may be more from “need” rather than “want” as 2 of the 3 were raising to pay down large amounts of debt in this high interest rate environment and Tempus in particular priced at a 40% discount to its last round valuation of $10B in 2022.

As seen elsewhere in the innovation ecosystem, exits remain sparse as later-stage digital health companies are trimming expenses and narrowing focus in a change to a more conservative stance rather than pursuing acquisitions for a “growth-at-all-costs” mindset. Fortunately, PE continues to do the heavy-lifting providing some reprieve and liquidity.

Canadian VC Overview

In Canada, VC investment activity for Q2 2024 jumped to $2.4B (up 85% from Q1) but across 143 deals (up only 12% from Q1) as 7 megadeals accounted for $1.7B of that. Adjusting for megadeals across both Q1 and Q2, the increase was a more “modest” 40% for deals under $50M in size between quarters. Deal volume has seemingly stabilized in Q2 compared to 2023 (145 in Q4 and 149 in Q3). Average deal value increased another 30% in Q2 vs Q1 to $13M, further supporting the narrative of a flight-to-quality with more money invested in fewer ventures.

Notably in Q2, Alberta has seemingly come out swinging (as may be recalled from past reports, anecdotal feedback from peers has been very bullish on Alberta deal flow) with ~$300M of deal value, a 3x increase over Q1; however, looking into the details, ClearSky’s $230M round accounts for most of this. Adjusting for this outlier, Q2 was down meaningfully from Q1. BC was also down in H1 2024 compared to H1 2023.

As usual, seperating the data out by investment stage and sector provides further – albeit not inspiring – context. Pre-seed and seed activity remains depressed in Q2 with only 26 deals and $18M invested compared to the ~$38M invested across 39 deals in Q2 2023. Average deal size reverted back and plummeted to $0.71M in Q2, >40% less than the five-year average of $1.35M. Seed deal volume remains more or less flat over the last few quarters at 53 deals (vs 51 in Q1) whereas average deal size increased to $2.56M from $2.38M in Q1.

Series A and B activity seemed frothy with >$1B invested across 41 deals (flat compared to 38 in Q1); however, this was largely driven by outlier company Waabi that raised $275M in Q2. Adjusting for Waabi, average deal size was up slightly to $18.7M from $15.3M in Q1.

We remain concerned over the Canadian VC ecosystem health as deal counts should be highest at the earliest stages of investment (top-of-funnel) to support attrition for further stages of investment and the risk-off behaviour of investors shifting to Series A and B funding rounds may in the future hinder the replenishment of new ventures. While this should be an overall concern for the ecosystem, this could provide Nimbus a bullish opportunity to win the highest quality opportunities in those earlier stages.

From a sector perspective in Canada, the ICT sector appeared to receive a breather from its recent precipitous fall after two megadeals helped elevate deal value with volume remaining flat in Q2. Conversely, Life Sciences retraced itself with deal value dropping 68% from Q1 despite deal volume remaining relatively flat.

Even in Canada: mixed signals.